A Theory of Lags

A Theory of Lags

We review CPI, and outline one theory as to why transmission lags may have lengthened

Summary

We review April’s CPI numbers. While not an un-alloyed positive, the balance of evidence from the release provides further cautious encouragement that inflation should continue to moderate going forward. In the second part of this note we outline a theory as to why lag structures may have lengthened in this cycle, based on evidence of shifts in how inflation expectations are formed. We discuss the implications of this hypothesis for markets.

April CPI Review: Another Encouraging Print

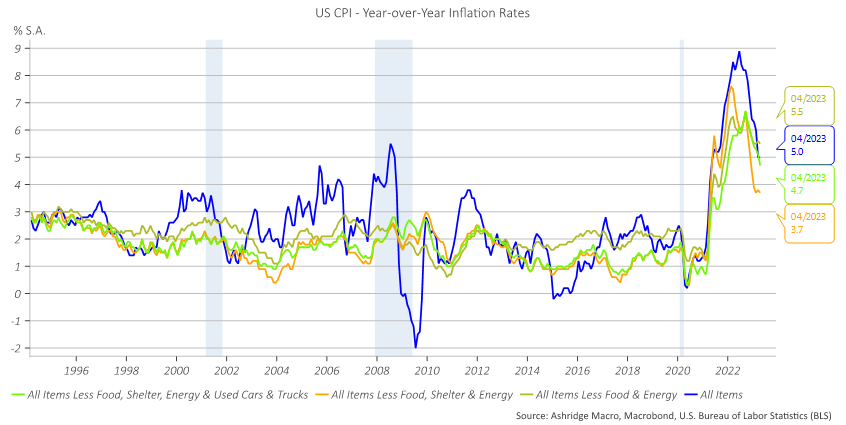

Headline and Core Run-Rates: Faster, but In-Line

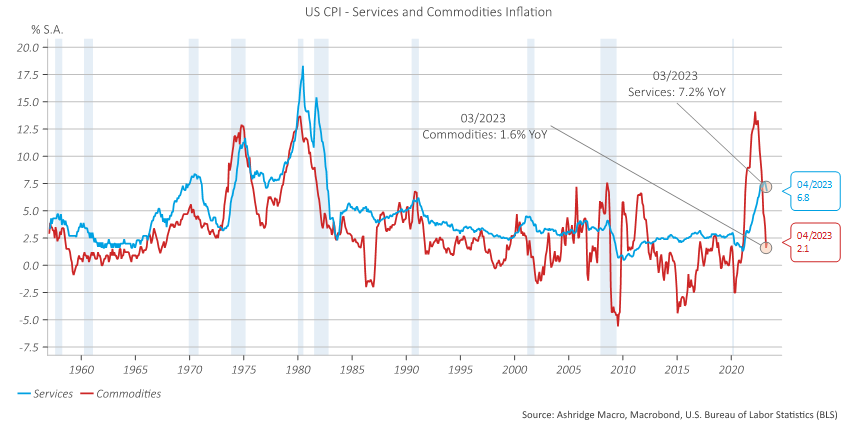

Headline CPI printed +40bps MoM in April, in line with the consensus, and on a year-over-year basis held constant at 5%. Core also printed +40bps MoM, essentially in line, and ticked down marginally on a year-over-year basis. The headline number was a firm re-acceleration versus the 10bps MoM run rate in March, with the reacceleration driven by an increased contribution from transportation subcomponents. Services inflation softened slightly, from a run-rate of 30bps MoM in March to 20bps MoM in April.

Drivers and Contributions: Faster Transportation, Recreation and OER

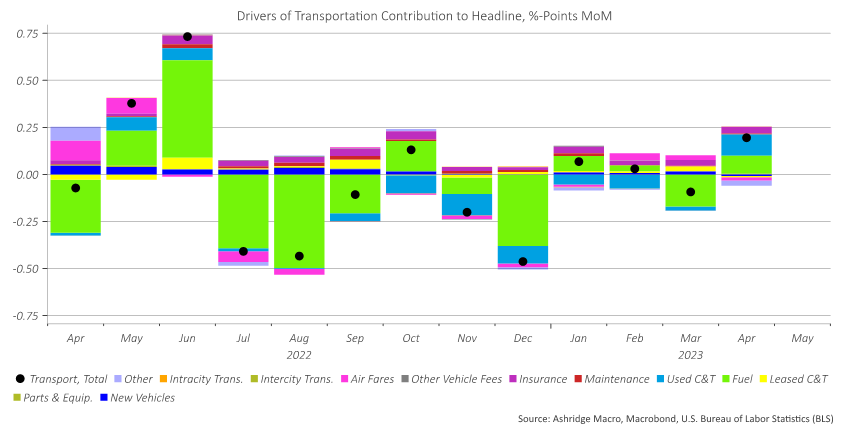

The reacceleration in the headline print was almost entirely driven by transportation-related subcomponents. Inflation in this category re-accelerated from -50bps MoM in March to +120bps in April, and the contribution of transportation to headline CPI consequently flipped from -9bps to +20bps.

In a typical month historically, fuel costs will explain a large share of the variance in transportation inflation overall. In April, the rebound in transportation was mostly driven by large rises in the prices of used cars and trucks, which had previously been dropping fairly consistently in earlier data.

The BLS estimates the inflation rate for used cars and trucks based on price estimates from JD Power. While slightly different in terms of definition and scope, the Manheim used vehicles index generally leads the official BLS numbers by around two months. The Manheim index spiked in February, but grew less forcefully in March and contracted in April. A projection for CPI used cars and trucks based off its own lags and lags of the Manheim numbers suggests that April’s forceful MoM growth rate is unlikely to be sustained – inflation in used car and truck prices, per the BLS’ methodology, should moderate again in the coming months.

OER remained stable at 50bps MoM, having broken out of its prior range in the March release. Rents accelerated slightly over the course of the month, printing at +60bps MoM in April – in March, rents had grown by 0.5%. On a year-on-year basis OER ticked up marginally, while rents remained stable. More timely private sector data continues to suggest OER should moderate through the remainder of this year.

Breadth of Price Pressures: Generally Encouraging

Keep reading with a 7-day free trial

Subscribe to Ashridge Macro to keep reading this post and get 7 days of free access to the full post archives.