Sussing Out Sweden, Part IV: Rates and FX

Sussing Out Sweden, Part IV: Rates and FX

The final part of our four-part Swedish deep dive.

In this section we outline observations on Swedish rates markets and the Swedish krona. This discussion is not intended as advice – Ashridge Macro is not authorized to provide investment advisory services and does not seek to do so. Readers should note the important disclaimer at the end of this document.

Riksbank Policy and SEK Rates / FX

Our thesis for the Swedish growth outlook is that overall growth in 2023 will be weak, and the housing market will remain a particularly salient point of weakness. However, there’s very little in that assessment that is unique to us – the market understands the headwinds and has had much time to price them. We also anticipate that data could be less bad then feared – leading indicators suggest a troughing in the near future and housing may have already front-loaded the impact of hikes. We therefore think the balance of risks is tilted towards data upsides versus a bearish consensus.

Riksbank policy has shifted further to the hawkish side and the undesirability of krona depreciation was emphasized very heavily in February. Elevated inflation and a still-tight labour market gives the central bank scope to tighten further in a way which supports the trade-weighted krona, and February’s meeting would suggest appetite to do so. A more hawkish Riksbank has already been priced, but may limit the scope for near-term SEK downside.

In general more concave pricing (e.g. a higher overshoot versus neutral, followed by cuts towards neutral) is currency positive, holding the level and slope of policy rate expectations constant. The critical open question is whether:

Markets will read Riksbank hawkishness as a policy mistake, undoing any positive read-through to SEK, or…

Hawkishness can prove a support as markets move away from a less starkly stagflationary interpretation of Sweden.

If our view around the skew of surprises in the data is broadly correct, concerns around Riksbank overtightening could mitigate over the coming months, and higher policy rates could therefore provide clearer support for SEK.

In rates, there could be the potential for:

Terminal rate pricing upside on data beats, potentially skewing towards a payer bias in SEK OIS.

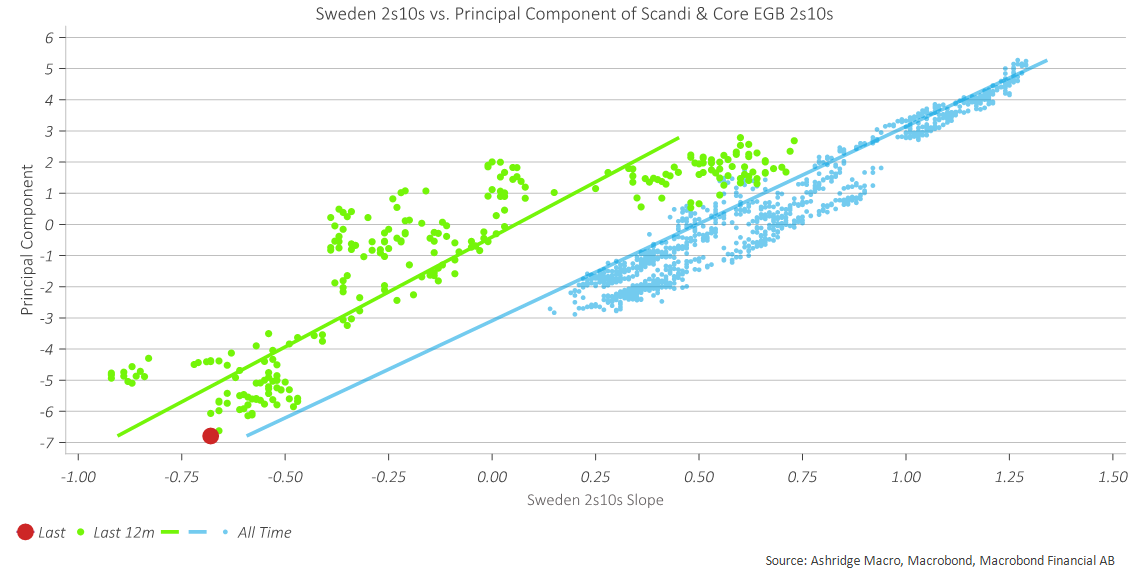

The SGB curve to range-trade with a flattener bias for now, as terminal rate pricing skew and the supply effects of Riksbank sales further out / data upsides partially cancel. We note that SGB 2s5s and 2s10s look marginally steep versus other Scandi and core EGB curves, which might lead to a near-term flattener bias. Bear steepening pressure can intensify later in the year as less supportive 2024 supply dynamics come into focus.

Overall bearish pressure on the front end.

Will Risk Kick the KIX?

As outlined in “Higher Rates, Fatter Tails”, our view around developed market growth in general is that strong Q1 data results in both tails of the 2024 growth outcome distribution fattening.

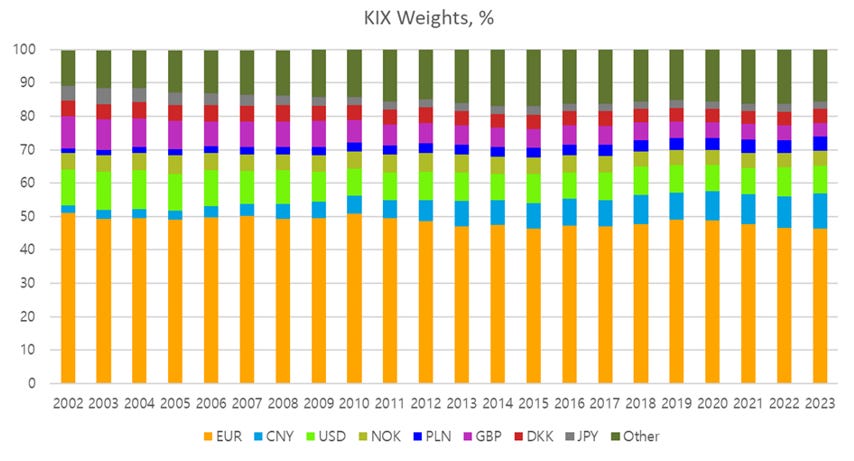

SEK is highly attuned to global risk dynamics – likely more so than to interest rate differentials. The skew of risk around the longer term global outlook, as well as the Swedish local outlook, therefore has the potential to disadvantage SEK versus havens like the dollar, franc and yen. Given these currencies’ relatively low trade shares with Sweden, a bilateral SEK depreciation versus havens on risk off is unlikely to be as troubling to the Riksbank as a further rally in EURSEK, which comprises around 46% of the KIX basket. A short bias on EURSEK may prove a more attractive way to position than a short bias on risk havens vs. SEK.

SGB Supply: Positive Near Term, Less Positive Further Out

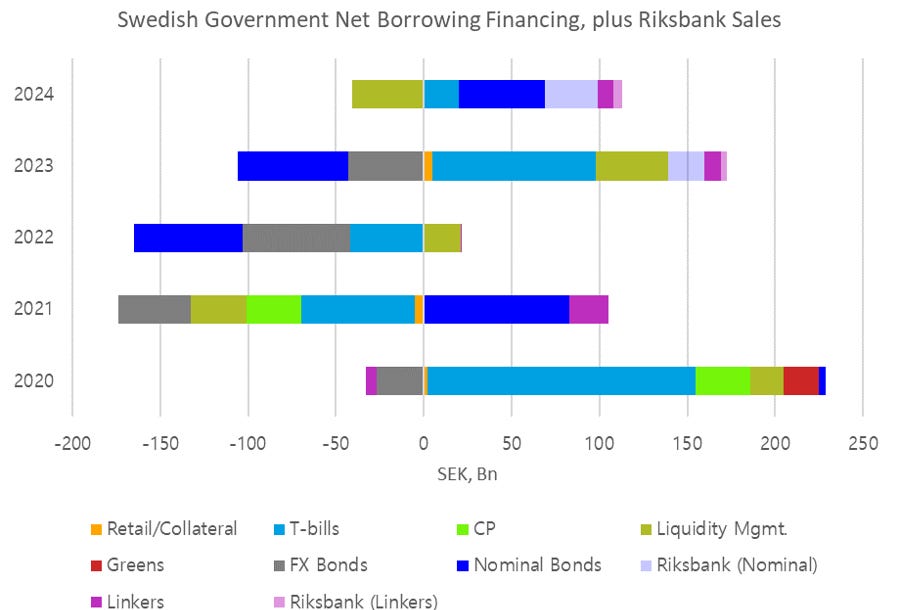

Swedish government financing requirements turn positive again in 2023, after 2022’s impressive surplus. Net borrowing this year is expected to be SEK41bn, which will fall to SEK37bn in 2024 (versus overall outstanding debt of around SEK1.11tn). Nevertheless, SGB net supply dynamics remain more supportive this year than next. 2023’s deficit is scheduled to be funded predominantly via bill issuance – net supply of nominal SGBs is projected to reduce by SEK63bn. In 2024 net nominal bond supply will be positive again - SEK49bn. Overall issuance dynamics look supportive for duration in 2023, but are likely to become less supportive as 2024 approaches.

A couple of risk factors also dampen the positivity of the supply backdrop.

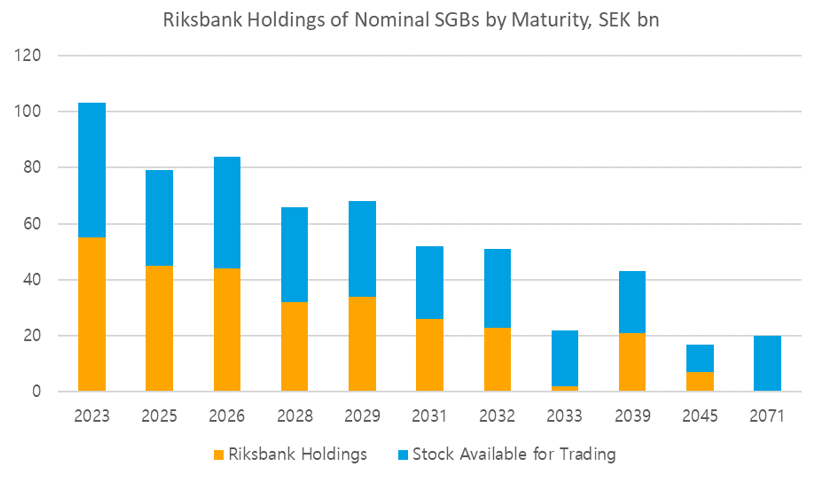

Firstly, the Riksbank’s active sales of SEK3bn nominals and SEK500mm reals per month from April (except for July and August) will add SEK21bn worth of effective supply to the SGB free float in 2023. The Riksbank will sell longer-dated bonds maturing from 2027 onwards.

Secondly, tail risks around Riksbank recapitalization remain. The Riksbank Act, which came into force in January, targets SEK60bn for Riksbank equity. Should Riksbank equity drop below 1/3 of its target, the Riksbank must petition parliament for recapitalization, and will generally receive recapitalization to bring its equity to 2/3 of the target level. Riksbank losses are realized at year-end[1].

Flows and Positioning

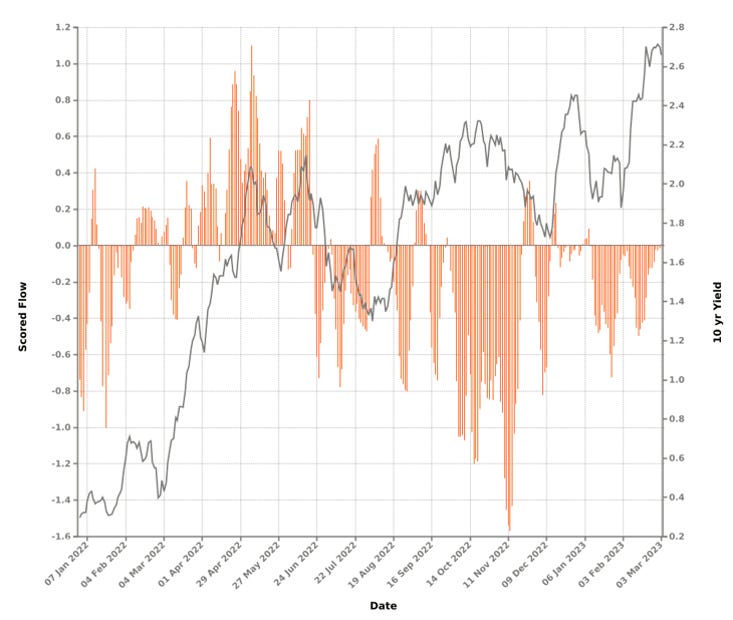

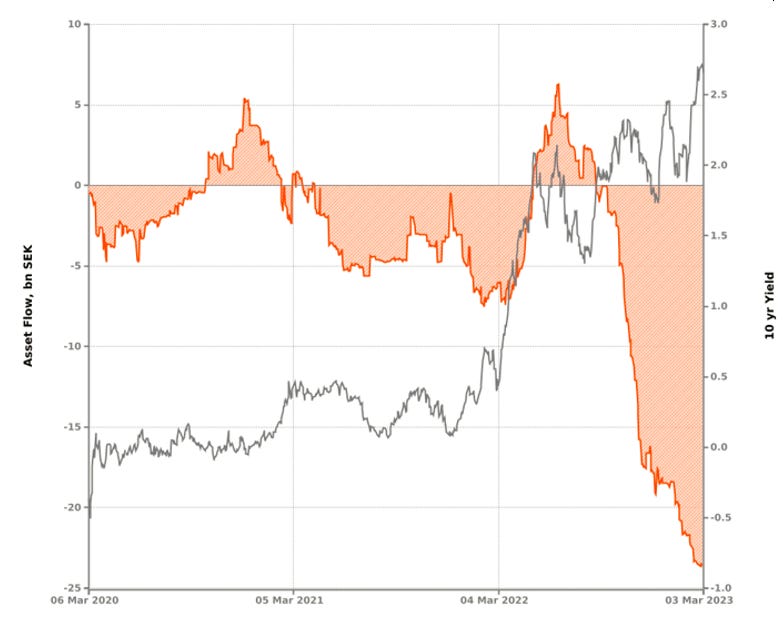

We examine flows and positioning using data from BNY iFlow. The first chart below plots smoothed inflows into SGBs, standardized versus typical levels, against 10y SGB yields (positive/negative Y-Axis values represent higher-than-average/less-than-average or negative flows). The second chart plots the cumulative sum of flows into SGBs since the start of 2020 in SEK.

Marginal SGB flows do not look extreme in either direction. A very pronounced selling bias has existed since 2021, and SGBs saw renewed selling pressure in the aftermath of the February Riksbank. However in more recent sessions the net flow has been essentially zero, suggesting this bias may be damping out. Cumulative SGB selling post H1 2022 looks very extreme versus recent history. Outstanding short exposure is likely to be profitable, and therefore vulnerable to profit-taking.

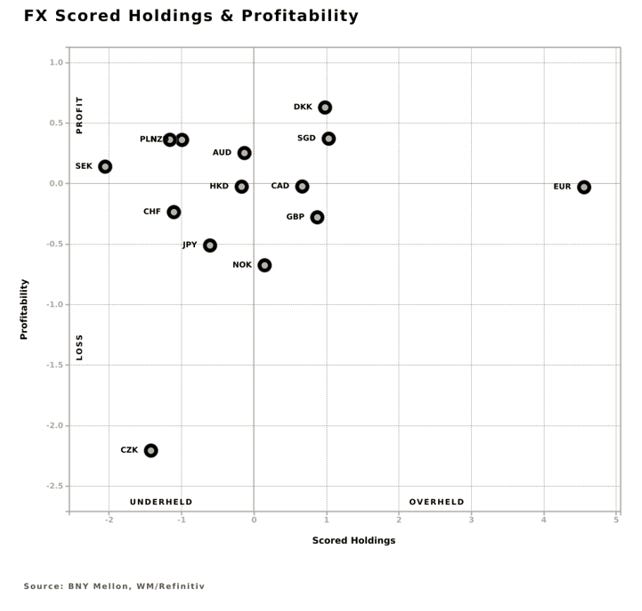

Turning to FX, the chart below tracks overall holdings (horizontal) and the profitability of those positions, backed out based upon the timing of the flow (vertical). SEK remains heavily underheld, with short positions profitable. EUR is heavily over-held, with positions close to breaking even. NOK is marginally overheld, with longs in the red. From a positioning standpoint, EURSEK looks vulnerable – profit taking on SEK shorts and an unwind of stretched EUR longs could contribute to a break of the very pronounced trend strengthening of EURSEK which has been in place since 2021.

[1] At year end 2022, Riksbank equity stood at SEK109.3bn – comfortably above all relevant thresholds, and sufficiently high to withstand a loss equivalent to the loss booked in 2022 repeating this year.